Understanding the Formula for the Future Value of an Ordinary Annuity

The formula for the future value of an ordinary annuity is a cornerstone concept in finance, helping individuals and businesses calculate the total value of a series of equal payments made at regular intervals over time. Whether you're planning for retirement, evaluating investment opportunities, or managing loans, this formula provides a clear picture of how your money grows with compound interest. In this article, we’ll break down the formula, explain its components, and demonstrate its practical applications with real-world examples.

The official docs gloss over this. That's a mistake.

What Is an Ordinary Annuity?

An ordinary annuity is a financial arrangement where equal payments are made at the end of each period. Common examples include monthly mortgage payments, car loans, or retirement savings contributions. And unlike an annuity due (where payments occur at the beginning of each period), ordinary annuities assume payments are made after the compounding period. This distinction is critical because it affects how interest accumulates over time The details matter here..

The Formula for Future Value of an Ordinary Annuity

The future value (FV) of an ordinary annuity is calculated using the formula:

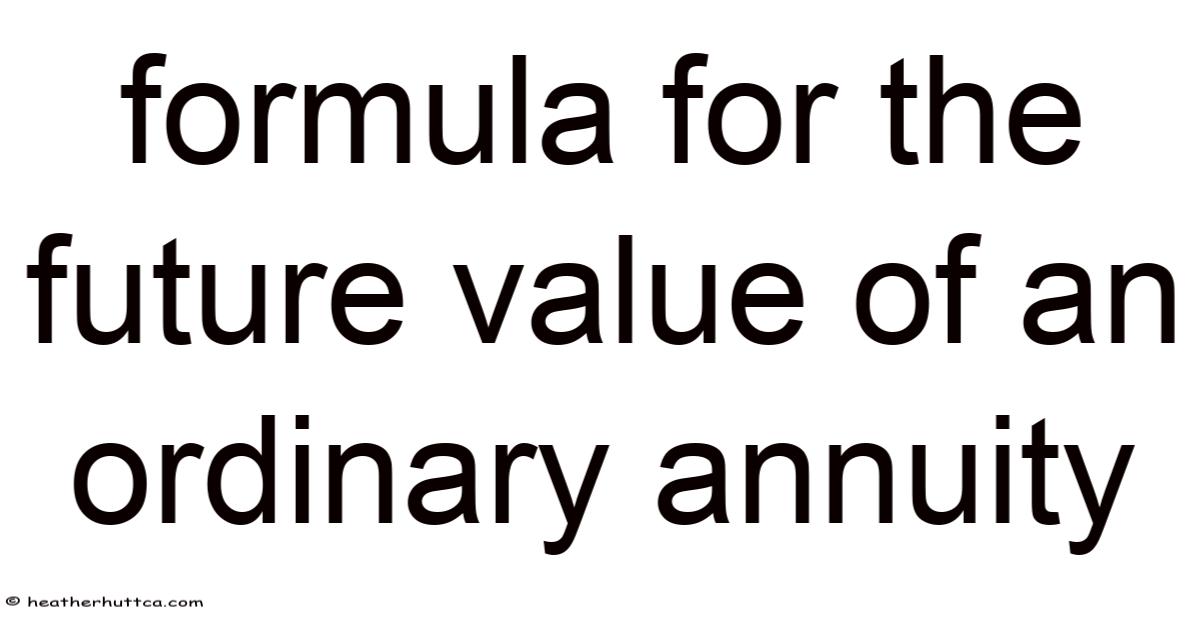

FV = PMT × [ ( (1 + r)^n – 1 ) / r ]

Where:

- PMT = Payment amount per period

- r = Interest rate per period (expressed as a decimal)

- n = Total number of payment periods

This formula accounts for the compounding effect of interest on each payment over time. Let’s dissect each component:

- (1 + r)^n: This part calculates the growth factor for compound interest over n periods.

- ( (1 + r)^n – 1 ): Subtracts 1 to isolate the interest earned beyond the initial principal.

- Divided by r: Adjusts for the periodic interest rate, ensuring the formula reflects the average growth of all payments.

Step-by-Step Example

Suppose you invest $1,000 monthly into an account that earns 6% annual interest, compounded monthly, for 5 years. Here’s how to calculate the future value:

-

Convert the annual interest rate to a monthly rate:

r = 6% / 12 = 0.5% = 0.005 -

Determine the total number of periods:

n = 5 years × 12 months = 60 periods -

Plug values into the formula:

FV = 1,000 × [ ( (1 + 0.005)^60 – 1 ) / 0.005 ] -

Calculate step-by-step:

- (1 + 0.005)^60 ≈ 1.34885

- (1.34885 – 1) = 0.34885

- 0.34885 / 0.005 = 69.77

- FV = 1,000 × 69.77 = $69,770

After 5 years, your investment would grow to approximately $69,770, demonstrating the power of compound interest.

Key Factors Affecting Future Value

Three variables drive the outcome of the future value calculation:

- Payment Amount (PMT): Larger payments directly increase the future value. Doubling your monthly contribution, for instance, will significantly boost your total savings.

- Interest Rate (r): Even small differences in interest rates compound dramatically over time. A 1% higher rate could result in thousands of dollars more in the long run.

- Time (n): The longer the investment period, the greater the impact of compounding. Starting early maximizes growth potential.

Real-World Applications

This formula is invaluable in scenarios such as:

- Retirement Planning: Estimating the growth of monthly contributions to a 401(k) or IRA.

- Loan Amortization: Understanding how much of your mortgage payments go toward interest versus principal.

- Investment Analysis: Comparing the future value of different investment options with varying rates and terms.

It sounds simple, but the gap is usually here.

As an example, if you’re choosing between two savings plans—one with a higher interest rate but shorter term, and another with a lower rate but longer term—you can use this formula to determine which yields a better return But it adds up..

Common Mistakes to Avoid

- Confusing Ordinary Annuity with Annuity Due: Payments made at the beginning of each period require a slightly adjusted formula.

- Incorrect Interest Rate Conversion: Always convert annual rates to match the compounding period (e.g., monthly, quarterly).

- Ignoring the Power of Time: Underestimating how extended periods amplify compound growth can lead to unrealistic financial projections.

Conclusion

The formula for the future value of an ordinary annuity is more than a mathematical tool—it’s a lens for understanding how consistent investments grow over time. By grasping its components and applying it to real-world scenarios, you can make informed decisions about savings, loans, and investments. Whether you

Whether you’re planning for retirement, saving for a major purchase, or evaluating investment opportunities, mastering this formula empowers you to take control of your financial future. Think about it: by consistently applying these principles and avoiding common pitfalls, you can harness the exponential potential of compound interest to build wealth over time. Start early, stay consistent, and let the math work in your favor.

The formula for the future value of an ordinary annuity is more than a mathematical tool—it’s a lens for understanding how consistent investments grow over time. By grasping its components and applying it to real-world scenarios, you can make informed decisions about savings, loans, and investments. Whether you’re planning

Honestly, this part trips people up more than it should The details matter here..

Here’s the seamless continuation and conclusion:

Whether you’re planning for retirement, saving for a child’s education, or building an investment portfolio, the future value formula provides clarity. Even so, it transforms abstract financial goals into actionable calculations, revealing the profound impact of disciplined contributions and time. Here's a good example: understanding how even small, regular investments can accumulate into substantial sums underscores the importance of consistency and patience.

Worth adding, this formula equips you to critically evaluate financial products. When presented with annuity offers, bond investments, or structured savings plans, you can cut through marketing hype and calculate the true long-term value. It demystifies how lenders structure loans and how insurers design annuity payouts, enabling you to negotiate better terms or choose options aligned with your objectives.

Counterintuitive, but true Small thing, real impact..

Avoiding the pitfalls highlighted earlier—such as misapplying interest rates or overlooking payment timing—ensures your projections remain accurate. A precise calculation prevents underestimating future liabilities or overestimating returns, safeguarding your financial strategy from costly errors.

Conclusion

When all is said and done, mastering the future value of an ordinary annuity formula empowers you to harness one of finance’s most powerful forces: compounding growth. It transforms regular, manageable contributions into exponential wealth over time, turning disciplined saving into financial security. Whether securing your own retirement, funding a legacy, or achieving short-term goals, this formula is your roadmap. By applying it thoughtfully, you make informed decisions that align with your vision, mitigate risks, and maximize opportunities. Remember: the math is straightforward, but its implications are life-changing. Start today, make use of time, and watch your financial future grow.

Understanding the mechanics behind compound interest and the future value of an annuity is crucial for anyone aiming to secure their financial future. This knowledge not only enhances your ability to plan effectively but also empowers you to make strategic choices that align with your long-term objectives. By integrating these concepts into your daily financial habits, you position yourself to benefit from the natural power of growth over time.

The process of calculating future value through this formula is more than a calculation—it’s a guiding principle for making decisions that resonate with your aspirations. Still, whether you’re evaluating investment opportunities or managing personal expenses, the insights gained here help clarify the path forward. This approach encourages mindfulness about timing, discipline, and the long-term consequences of your actions Worth keeping that in mind..

Embracing this methodology can also encourage a deeper awareness of financial literacy, enabling you to deal with complex scenarios with confidence. Practically speaking, it bridges the gap between theoretical knowledge and practical application, ensuring your efforts translate into tangible results. As you refine your understanding, you’ll notice how each step contributes to a stronger, more resilient financial foundation.

In the end, the journey toward financial stability is shaped by consistent effort and informed decisions. By leveraging the power of compounded growth, you access possibilities that might otherwise remain out of reach. Let this guide your path, shaping a future where your aspirations become reality Easy to understand, harder to ignore..

Conclusion

By integrating these principles into your financial strategy, you reach the full potential of your savings and investments. The seamless application of the future value formula not only strengthens your planning but also reinforces the value of patience and precision. Embracing this approach ensures that every contribution matters, setting the stage for a prosperous and secure tomorrow Small thing, real impact. Took long enough..